A little too long, if you prefer to own your house rather than rent it 'almost forever' from a bank.

U.S. President Trump recently pushed this muchlonger mortgage into the spotlight, as a way to lower payments for everyday homeowners. But here in Canada, a 50-year mortgage isn't likely to be measured into existence. With 25 years as the standard, getting a 30-year mortgage (or longer) is reserved for select situations.

Here's what the mortgage math shows for just how much a 50-year mortgage in Canada could end up costing you.

Key Points:

Lower payments, but interest costs can more than double what you'll pay for the home.

Equity grows very slowly as the majority of interest is paid earlier.

Amortizations in Canada have been reduced — so a 50-year option is unlikely.

Pre-payments or lump sums can reduce interest costs, no matter the amortization.

Dan Eisner, True North founder and CEO underscores the core risk:

"Having a 50-year amortization really means you could die with a mortgage. So many Canadians use their home as their life savings, and this is not a good business plan. It's not a good retirement plan. It's not a good financial plan. For many, it's a debt-trap scenario."

– Excerpt from an interview on Village Media's A Closer Look podcast, 50-year mortgage episode, aired Nov. 14, 2025.

Watch Dan's interview in A Closer Look podcast below:

Why might you consider a 50-year mortgage?

A longer amortization of 50 years means you'll stretch your mortgage payments over twice as long compared to a standard 25-year home loan.

That big stretch could mean a significant reduction in your monthly mortgage payments — up to about $700 per month less for a $500,000 mortgage, assuming a 4.0% 5-year rate — but you'll also more thandouble how much you'll end up paying for the home by the end.

First-time home buyers are just trying to get into the market. If they have a choice, they'd likely take that 'attractive' mortgage budget despite the financial consequences, thinking perhaps they'll be able to pay it down later.

Dan explains: "Someone who wants to realize their dream of owning a home will say, 'Who cares if I pay for this for the rest of my life. At least I own it, right?', and they'll place that ability to afford the payments over the risk of paying a lot more interest. The knock-on effects for individuals, lenders, and the economy would start racking up fast."

How do payments and interest costs change with a 25, 30, and 50-year mortgage?

Based on an original mortgage balance of $500,000 and a 5-year rate of 4.0% over the entire mortgage loan:

25-yr

30-yr

50-yr

Monthly Payments

$2,630

$2,370

$1,910

Difference w/ 25-yr

-$260

-$720

Percentage

-10%

-27%

Overall Interest Cost

$289,030

$355,933

$650,585

Difference w/ 25-yr

+$66,903

+361,555

Percentage

+23%

+125%

Note: Amounts are approximate. Over the life of a mortgage, rates will change, affecting payments and the interest paid. Interest rates for 30- and 50-year mortgages may be higher than those for a standard 25-year mortgage, because lenders take on more risk.

The problem with ultra-long amortizations.

The biggest problem for a 50-year mortgage is time, even though it's the reason for lower mortgage payments.

Given that the average age of first-time home buyers in Canada is around 30 years old (CMHC, May 2025), a 50-year mortgage suggests not only that the mortgage may not be paid off in the homeowner's lifetime, but also that it could leave mortgage debt for beneficiaries to handle.

The long mortgage amortization can mean:

Total interest costs balloon.

Home equity builds at a crawl in the early decades.

Feeling 'locked in' to a never-ending loan.

Being limited by a higher debt load for other borrowing or repayment needs, such as a car loan or further education.

More difficulty managing mortgage payments if income drops later in life or in retirement.

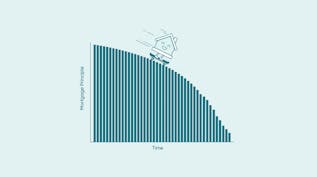

You pay a majority of the interest in the first couple of decades.

As the graph below shows, the majority of the interest for a 50-year mortgage is paid off within the first 20-ish years.

What does it mean for your financial health? It means that as the decades wear on, you have less access to home equity because you're paying down the mortgage principal more slowly compared to a 25 or 30-year mortgage — impacting your ability to refinance for extra funds you may need.

Or if you sell your home early to pay off the loan, you'll have much less of the money you've paid into it to use for other purposes, like buying another home.

What if you want the lower payment — but plan to pay the mortgage off sooner?

"In 2025, about 25% of our THINK Financial clients paid extra down on their mortgage principal through their pre-payment feature." – Dan Eisner

A 50-year mortgage could make sense if you have access to extra funds within the first 10-15 years, and it would depend on your lender's pre-payment privileges.

For example, True North's in-house, CMHC-approved lender, THINK Financial, offers a 20% annual pre-payment privilege (lump-sum or additional payments that go directly to the mortgage principal):

For a $500,000 mortgage, if you have access to an extra $100,000 annually, your mortgage could beentirely paid off in 5 years, regardless of original amortization.

Most Canadian homeowners don't typically have access to those kinds of funds. But say you can scrape together an extra $25,000 annually to put toward your 50-year mortgage (with a 4% fixed mortgage rate)?

Then, it would take only about 14 years to pay it off in full (72% faster), and instead of paying about $655,500 in interest, you'd pay only about $155,000.

In this scenario, not only would you get extra monthly cash flow of about $700, but you'd save a ton of interest. But that raises the question — if you have all that cash, is a 50-year mortgage that helpful?

As you can see, it's harder to make the mortgage math work well with such a large, long-term (50-year) home loan.

What amortizations can a Canadian homeowner access right now?

The standard mortgage amortization in Canada is 25 years:

A default-insured mortgage (less than 20% down payment of home purchase price) can be stretched to 30 years if you're an eligible first-time or newly-built-home buyer.

Uninsured mortgages (with a 20% or more down payment) may be able to stretch the loan term to 30 years.

Over 30 years typically requires approval with an alternative or private lender and comes with higher mortgage rates.

Longer amortizations were once allowed, with some able to extend to 40 years with a traditional lender. However, the Canadian banking regulator battened down those hatches as it became clearer that lenders and homeowners were being overexposed and overextended.

A quick look at Canada’s amortization rules.

A 25-year mortgage is today's standard for homeowners, but it hasn't always been. Insured mortgage amortizations were tightened over time: from 40 years in 2006 to 35 in 2008, then 30 in 2011, and to the current 25-year limit in 2012.

As of December 2024, some first-time and new-build buyers can again access 30-year insured options.

Uninsured mortgage amortizations may extend to 30 years, depending on the details and lender. Longer options of 35 or 40 years are generally only available through an alternative or private lender.

Instead, get a wonderful, very good mortgage.

The 50-year mortgage, while not a realistic option for Canadian homeowners (this product exists on the commercial real estate side for multi-family complexes), does raise interesting points.

If you do decide to extend your amortization for lower payments to get into your first home, or when renewing your mortgage — putting even a little extra down on your mortgage principal, especially in the early years, can help you save on interest overall.

Even changing your payment frequency (hopefully with no extra fee) can cut your interest costs and shorten your mortgage timeline.

Here at True North, our expert, salaried brokers put you first to help you reach your homeownership goals. We outline your options, in your preferred language, to help you make clearer, more confident decisions based on your unique situation.

And we have access to multiple lenders and volume rate discounts for a simple, stress-free process that can save you thousands.

Anywhere you are in Canada, give us a shout for all your mortgage needs. We're available online, over the phone, by email — or drop by a True North store near you.