Will the trade war cause a recession in Canada?

Canada's economy already contracted during the second quarter of 2025, with GDP (Gross Domestic Product) declining at an annualized rate of -1.6%. All three months in the quarter logged a decrease, with April, May and June each contracting by 0.1% year-over-year.

(A technical recession is considered two quarters of contraction in a row, though not all economists agree with this definition.)

Contrast that negative print with +2.6% annualized growth at the end of last year and +2.0% at the start of this one, and it's clear that the trade war chaos is weighing on Canada's economy.

Could a prolonged recession emerge? Economists remain split — some expect meagre growth to return and stay sluggish through year-end, while others warn that continued higher tariffs and job losses could deepen the downturn.

Economic disruptors take time to show up in the data. This year's fresh trade war with the U.S. is ongoing and still being reflected in company spreadsheets and business results, with GDP readings lagging by two to three months.

As a slowdown increasingly becomes apparent, the Bank of Canada is likely already adjusting its potential rate path, while keeping a close eye on inflation (its primary focus in steering the economy).

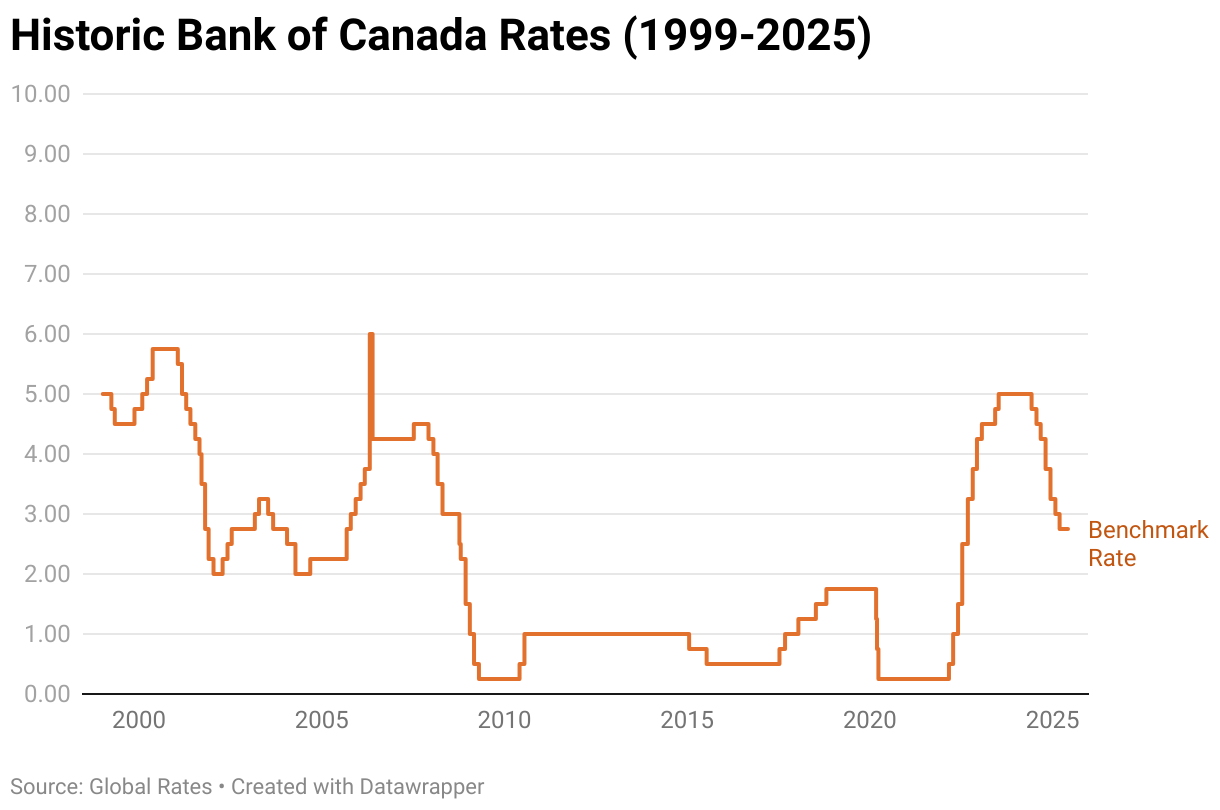

How low could rates really go?

Many Canadian economists, such as those from RBC, BMO, TD, and National Bank, and our own True North Founder and CEO, Dan Eisner, generally agree that the BoC is in a position to cut rates — but not all the way back to a rock-bottom 0.25% (at least, not yet).

Dan explains, "The trade disruption is certainly an unexpected blow this year, but for rates to head that far down, there also needs to be widespread consumer pullback along with core inflation that's lower than the BoC's target. Another rate cut or two is likely to support a demand upturn, perhaps enough to stave off a full-blown recession as companies adjust to new trade realities."

Interest rates will likely remain higher due to inflationary pressures from the very tariffs that are causing the economic cooling. Consumer demand barely eased in Q2, despite negative growth — though if it finally cools, inflation may also declibe, allowing for more rate cuts if the economy demands it.

Recession and Rate Scenarios:

- Mild recession: Rates could drift downward to 2-2.25% (from a current BoC policy rate of 2.50%).

- Deeper recession with global fallout: Only then could BoC test the lower bound on its policy rate once again.

What could keep rates from hitting rock bottom this time around?

One past recession is not like another possible (future) recession. This time, inflation risks are pushing harder against the weakening factors, complicating rate reductions.

Several conditions could keep mortgage rates higher than historic lows:

- Sticky core inflation driven by consumer demand resilience, tariff-driven cost pressures, and government spending.

- Government support of trade-impacted sectors.

- BoC will be cautious of re-igniting demand too soon.

- Renegotiated trade agreements could lead to reduced business pressures.

- New national and international trade markets may help replace lost U.S. business.

- National infrastructure projects and reduced inter-provincial tariffs could spur growth.

- Canada's population gain is slowing, which may help moderate the labour market strain.

What could clear a path to rock-bottom rates?

Here are some factors that could see Interest rates and mortgage rates revisit the floor:

- Trade wars and higher tariffs hit exports harder (or register greater impact over time).

- Canada faces multiple quarters of GDP contraction (like in 2008–09).

- Consumer demand and housing activity slow in tandem.

- Unemployment hits 8%.

- Inflation remains below the Bank of Canada's 2% target.

- Global growth stalls at the same time.

An escalation of global conflict could add fuel — through higher oil prices and new supply-chain shocks — amplifying the drag from disrupted trade relationships.

And all of these factors would need to sufficiently overwhelm any government stimulus that might otherwise cushion the blow.