Posted Rates vs Actual Rates

Is the rate you see, the rate you get? Not always, and here's why.

Mortgage Rate Forecast (2026-2030)

Continually updated. Where rates may go now and later — and what’s driving them.

How Government Bond Yields Relate To Mortgage Rates

Want to know where fixed rates are going? Watch bond yields.

Housing Market Forecast (2026-2029)

Continually updated. Get an idea of the housing outlook and interesting deets.

Celebrating our 20th Anniversary!

For 20 years, we've granted your wish for a better rate. See how we've grown!

Your Summer Home Maintenance Checklist

Need another excuse to get outside? Here's 10. Read our tips now!

Ontario HST Rebate: One Year Window

For eligible buyers of newly built homes, a full HST rebate is proposed for a limited time.

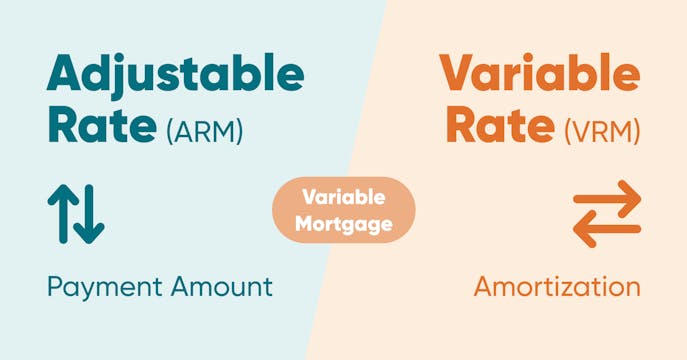

What is an Adjustable-Rate Mortgage?

Payments that change along with the prime rate may be better for your long-term mortgage savings.

Prime Rate Impact on Mortgages: Explained

The prime rate sets the temperature for your mortgage costs. Learn more.

Should you choose a variable rate in 2026?

How to decide between variable-rate FOMO or JOMO? We can help.

GST Rebate on New Homes: How It Works

First-time buyers of newly built homes now qualify for a 100% federal GST rebate — up to $50,000.

Mortgage Stress Test: What is it and how does it work?

This test helps ensure you can handle higher payments as an affordability buffer.