Mortgage Rate Forecast (2026-2030)

Continually updated. Where rates may go now and later — and what’s driving them.

How Government Bond Yields Relate To Mortgage Rates

Want to know where fixed rates are going? Watch bond yields.

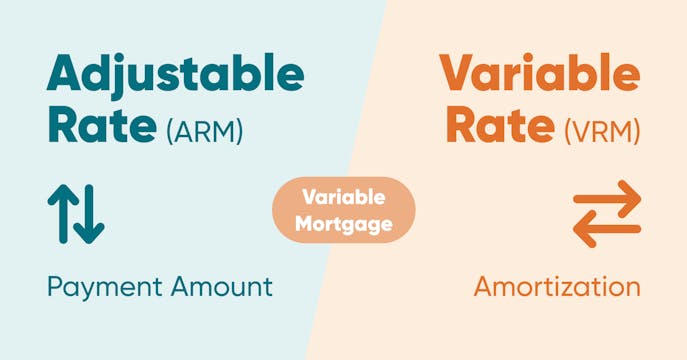

What is an Adjustable-Rate Mortgage?

Payments that change along with the prime rate may be better for your long-term mortgage savings.

Prime Rate Impact on Mortgages: Explained

The prime rate sets the temperature for your mortgage costs. Learn more.

Should you choose a variable rate in 2026?

How to decide between variable-rate FOMO or JOMO? We can help.

GST Rebate on New Homes: How It Works

First-time buyers of newly built homes now qualify for a 100% federal GST rebate — up to $50,000.

Mortgage Stress Test: What is it and how does it work?

This test helps ensure you can handle higher payments as an affordability buffer.

Keeping Track of Mortgage Rule Changes

Do recent rules affect your mortgage decisions? See recent and past changes.

Housing Market Forecast (2026-2029)

Continually updated. Get an idea of the housing outlook and interesting deets.

2025 Mortgage Year is Wrapped!

An eventful 2025 year in review — here's our playlist of the (mortgage) highs and lows.

2026 Housing Stats

Get to know the latest Housing Market trends to inform your buying and selling decisions.

Proof that our rates are lower.

Our rates are 0.18% lower on average compared to everyone else. Prove it? Okay!