Read the article! Our expert broker, Victor Tran (Mobile Mortgage Broker), talks about the mortgage sweet spot in Rob Carrick's July 17, 2023 Globe and Mail article.

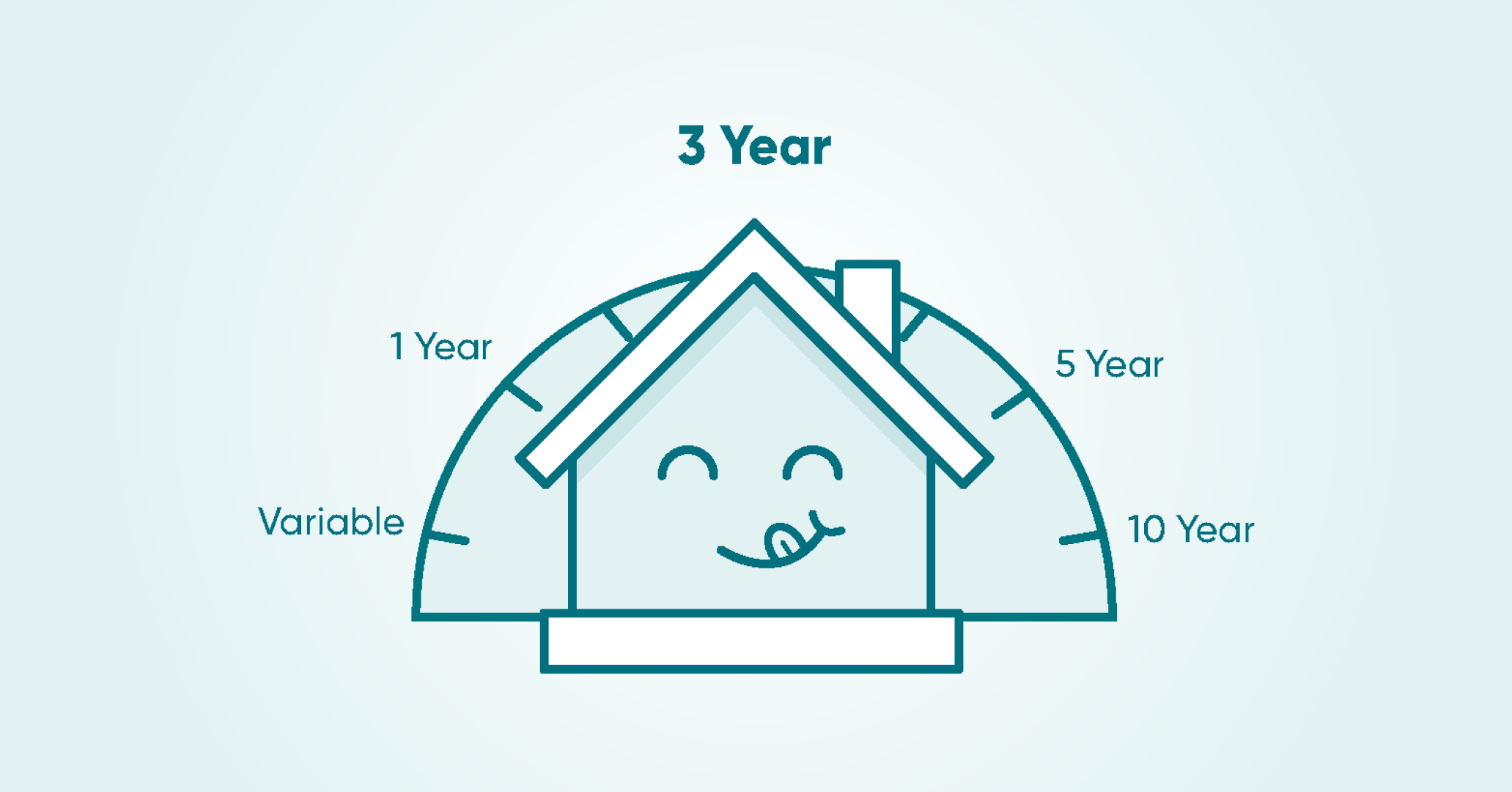

Can short-term mortgage rates save you money?

Getting your best deal on rates doesn't always mean choosing a (longer) 5-year term.

Here's when choosing a shorter term of 1 to 4 years might benefit you, and when it might not.

Go short? This middle ground for rate-risk may save you cash.

At True North Mortgage, we're seeing more home buyers and owners choose shorter mortgage terms that can offer a middle ground for rate-risk:

- 5-year variable mortgage rates have shot up in the last year, making them a higher-risk choice for tight budgets.

- With the Bank of Canada's recent rate hikes possibly making a dent in high inflation, rates are anticipated to start dropping in a year or so.

- 5-year fixed rates, usually the choice for low-risk appetites, now carry an increased risk of paying a higher rate for longer.

- Breaking a 5-year term to take advantage of declining rates may incur costly penalties.

- Right now, shorter terms, such as 2 and 3-year fixed rates, may come with a slightly higher rate but offer the chance to renew earlier and penalty-free into (anticipated) lower rates to save more.

The popular 5-year term (for both fixed and variable rates) can offer a great rate while reducing time and stress in managing renewals. But with Canada's post-pandemic market mayhem, many of our clients are taking a closer look at shorter terms.

The 3-year term is today's (mortgage) sweet spot.

Long-time True North Mortgage Broker (in Toronto, ON), Peter Esper, has seen a substantial uptick in his clients choosing shorter terms among today's higher mortgage rates:

"I’ve been getting lots of deals recently – I’d say this week I’ve sent in almost 20 deals and most are going with the 3-year term. The 1 and 2-year terms are much higher on the rate at the moment — plus there’s still some volatility in the market, so the 3-year mortgage is the sweet spot.

In 3 years, rates are highly-anticipated to be lower, so clients will likely be renewing into a lower rate and payment to save more than choosing today's 5-year fixed rate.

I advise them that if they’re already used to that payment amount and can manage to keep it as-is, their interest savings will go directly toward their mortgage principal, paying off their mortgage years quicker and saving them even more on interest costs."

Current economic volatility, especially with the recent U.S. bank failures' effect on the Canadian bond market, is placing shorter terms in an upfront position to see mortgage holders through to calmer markets and lower rates. Today it may be the 3-year term, but 1, 2 or 4-year rates may also offer better options than a 5-year term for the next while.

That's why Peter says he supports his clients "both with short-term decisions and the long-term picture" for the best mortgage-savings strategies to help them reach their financial goals.

A short-term rate is appealing to more than just Peter's clients.

True North Mortgage, as a whole, has seen a dramatic change in clients choosing shorter terms over the past 6 months:

True North Mortgage, Terms Chosen (Sep. 2022 to Feb. 2022):

Over 44% increase in 1 and 2-year fixed-rate mortgage terms

Over 140% increase in 3 and 4-year fixed-rate mortgage terms

A decrease of 44% for a 5-year fixed-rate mortgage

A decrease of 84% for a 5-year variable-rate mortgage

What are the benefits of choosing a shorter-term fixed rate?

- If rates go down, you could renew into a lower rate sooner.

- Even if your short-term rate is higher (than a 5-year fixed), you may still save more by renewing into a lower rate earlier.

- The average Canadian homeowner only makes it to 3.89 years (of their 5-year term), so you may save even more by avoiding paying penalties and fees with a shorter term.

- You'll save instantly if short-term rates are lower than a 5-year term (which is often the normal state of rates).

- In a higher-rate environment, your lowest rate on a 5-year mortgage may still end up costing you more if rates go lower during your term.

- Compared to the higher risk of a variable rate, a short-term fixed rate may provide more payment certainly while allowing an earlier opportunity to change your rate.

- During a time of rate volatility, you may get peace of mind riding it out with a shorter-term rate.

What are some downsides to a short-term mortgage?

- You'll renew sooner, which takes time and may cause stress (though our expert brokers work hard to make it simple).

- If rates go up, you'll pay a higher rate sooner.

- If short-term rates are higher (than a 5-year variable or fixed), you'll pay more interest during your term.

Surfing shorter terms could help you save more over the life of your mortgage.

During more economically-stable times, short-term fixed mortgage rates tend to be lower than 5-year fixed rates. That's because the term contract is for less time — the lender's costs are lower, there's less risk that you'll default, and they don't mind the chance you'll pay a different rate sooner.

So, if you keep locking in with a low, shorter-term mortgage rate, it can offer the benefit of knowing your rate and payments are fixed while saving cash. And you'll have the opportunity to make a change or possibly renew into even lower rates earlier, penalty-free.

A shorter-term strategy may offer you a middle-ground of risk to average out more savings over the life of your mortgage. It's not as 'high-risk as riding out the ups and downs of a variable-rate term and may offer increased savings over the 'safer' 5-year fixed term.

Where are rates going? Peter Esper, senior True North broker, sees rates possibly dropping back to the 3.0% range by 2025/26. Dan Eisner, True North CEO, also talks about what's behind the latest central bank rate pause — check out his 2023 Mortgage Rate Forecast.

What are our current short term rates?

Get a lifetime of rate help.

Our highly trained, salaried, unbiased True North Mortgage brokers know the rate trends, and can help outline the right details for your clearer decision.

Every mortgage is different, and your needs are unique. We'll help you decide what level of risk suits your situation — and offer your lowest-possible rate with flexible mortgage options to help you save thousands.

On your behalf, we quickly search accredited lenders and thousands of products, informing you of rate specials or deals on short and long-term rates. Plus, our in-house lender, THINK Financial, is proven to have rates that are 0.18% lower on average compared to the competition.

Anywhere you are in Canada, get pre-approved fast to hold your rate for up to 120 days. We can help you easily online, over the phone, at a store near you, or one of our Mobile Brokers can come to you.

Short-term savings, long-time mortgage support.

The 'rate' advice you need.

Proof that our rates are lower.

Our rates are 0.18% lower on average compared to everyone else. Prove it? Okay!

Worried about your renewal?

Higher rates painting you into a budget corner? Get help to find a way out.

Watch Out For Mortgage Traps

Is your spidey-sense tingling? Watch out! That bargain-bin rate may cost you more later.